Introduction:

Graeme Colley, who is a well-known expert in SMSFs and the Cloudoffis Independent Consultant, has provided an update on the latest developments for Div 296.

Understanding Division 296 from what we know

The reworked Division 296 legislation, Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026, finally made it to parliament in February this year after going through many changes since it was announced in the 2023-24 Federal Budget. The main changes in the bill are a move away from taxing unrealised capital gains and the indexation of the thresholds. There are a number of other important changes that have taken place and should be understood if the legislation finally makes it into law.

The current bill continues to reduce superannuation tax breaks for anyone with a total super balance of more than $3 million and places an additional impost on those with balances of more than $10 million. An individual’s realised fund earnings from 1 July 2026 is taxed if their total super balance for Division 296 purposes is above the relevant threshold.

The main features of the bill are:

- The legislation is proposed to commence on 1 July 2026 rather than 1 July 2025 as originally proposed.

- For anyone with a superannuation balance of $3 million or more the tax will be a maximum of 15% of the realised income for the relevant financial year. If a person has a superannuation balance of $10 million or more there is an additional impost of 10% on the realised income.

- The realised income is based on income tax principles rather than the concept in the original proposal which taxed the difference between the individual’s opening and closing superannuation balances for the year. It is calculated at the fund level and an amount is attributed to the relevant member. For an SMSF it is expected an actuary will make the calculation.

- Trustees of SMSFs will have the option of resetting the cost base of the fund’s investments as at 30 June 2026 to recognise the level of accrued value in the investment to that time. The option is only available on all of the fund’s investments and applies only for purposes of Div 296.

-

The calculation of Div 296 tax consists of three stages:

- Stage 1 – Percentage formula (s 296-40(2))

- Stage 2 – Div 296 fund earnings (s 296-45(2))

- Stage 3 – Taxable superannuation earnings (s 296-40(1))

- Division 296 tax is levied on the individual who has the option of paying the tax from their own resources or having the superannuation fund pay the liability.

Stage 1 – the percentage formula

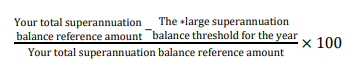

The percentage formula determines the proportion of a person’s balance that is above each of the thresholds. There is one formula for calculating the proportion above $3 million and another which calculates the proportion of a person’s balance above $10 million.

The formula that applies where the person’s total superannuation balance is at least $3 million is:

Where:

The total superannuation balance reference amount is the greater of a person’s total superannuation balance (if any):

• just before the start of the year; and

• at the end of the year.

The large superannuation balance threshold is $3 million (or indexed threshold) for the year.

Note: for the 2026-27 financial year (the first year of operation) the year end figure will be used in the calculation.

The examples of Judi and Brad illustrate how Division 296 tax will be calculated for someone who has a total superannuation balance of greater than $3 million in the case of Judi and in the case of Brad, $10 million.

Example

Judi has a Total Superannuation Balance (TSB) of $4 million on 30 June 2027 and a TSB of $3.5 million on 30 June 2026. Her total superannuation fund earnings for the year is $100,000 which means she will have a tax liability for Division 296 purposes.

As Judi’s TSB on 30 June 2027 is $4 million it will be used to calculate the percentage of her TSB that is over and above her large superannuation balance.

The proportion of Judi’s TSB above the $3 million threshold is 25% which is calculated as:

Total Superannuation Balance above $10 million

The second formula which is used to calculate the additional tax impost on TSBs above $10 million is:

Where:

The total superannuation balance reference amount is the greater of a person’s total superannuation balance (if any):

• just before the start of the year; and

• at the end of the year.

The very large superannuation balance threshold is $10 million (or indexed threshold) for the year.

Note: for the 2026-27 financial year (the first year of operation) the year end figure will be used in the calculation.

Example

Brad has a TSB of $12 million as at 30 June 2027 and a TSB of $10.5 million on 30 June 2026. His total superannuation fund earnings for the year is $1,000,000 which means he will have a tax liability for Division 296 purposes. As Brad’s TSB is greater than the very large superannuation balance of $10 million he will be required to pay additional tax.

The proportion of Brad’s TSB above the $3 million threshold is 75% which is calculated as:

The proportion of Brad’s TSB which is above the $10 million threshold is 16.67% which is calculated as:

Stage 2 – Div 296 Fund earnings

Stage 2 determines the fund earnings for Division 296 purposes which is calculated at the fund level not the member level. Once the fund earnings has been determined a further calculation is made to work out the amount of fund earnings that applies to the member. At this stage (as at 19 February 2026) the method used to calculate the member amount is not available as it will be included in the regulations if the bill becomes law.

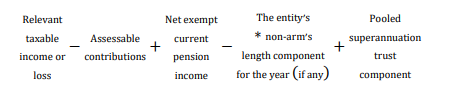

The formula to determine the fund earnings is:

Where:

Relevant taxable income or loss is the fund’s taxable income for the year,

Assessable contributions are the taxable contributions included in the fund’s income for the year,

Net exempt current pension income is the fund’s exempt income less the total deductions if the exempt income was assessable income.

The entity’s non-arm’s length component for the year (if any) is the amount of income that is taxed as NALI by the fund.

Pooled superannuation trust component applies if the fund has an investment in such a trust.

Example – Judi

Using the example of Judi above the fund’s taxable income is $350,000, assessable contributions claimed by the fund are $60,000 and the fund’s net current pension income less expenses is $310,000. The fund does not have any non-arm’s length component or investments in a pooled superannuation trust. Therefore the fund earnings for Division 296 purposes is $600,000. It is determined by an actuary (as proposed) that the proportion of the Div 296 fund earnings attributable to Judi is $100,000.

Example – Brad

The Div 296 fund earnings attributable to Brad has been calculated as $1,000,000.

Stage 3 – Taxable superannuation earnings

Taxable superannuation earnings is calculated as:

The percentage amount ×the Div 296 fund earnings

which involves multiplying the percentage amount from Stage 1 by the Div 296 fund earnings calculated in Stage 2.

Example – Judi

Judi’s taxable superannuation earnings is calculated as:

25% ×$100,000=$25,000

The amount of tax payable on Judi’s large superannuation balance is:

$25,000 ×15%=$3,750

Example – Brad

Tax on Brad’s large superannuation earnings

Brad’s taxable superannuation earnings is calculated as:

$1,000,000 ×75%=$750,000

The amount of tax payable on Brad’s large superannuation earnings is:

$750,000 ×15%=$112,500

Tax on Brad’s very large superannuation balance earnings

Brad’s very large superannuation earnings is calculated as:

The percentage amount ×the Div 296 fund earnings

The percentage amount on Brad’s very large superannuation earnings is 16.67% and Brad’s superannuation earnings is $750,000. Therefore the amount of tax payable on Brad’s very large superannuation balance is:

16.67% ×$750,000=$125,025

The amount of tax payable on Brad’s very large superannuation earnings is:

$125,025 ×10%=$12,502.50

The total Div 296 tax payable by Brad will be:

$112,500+12,502.50=$125,002.50

The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 is yet to be debated in both houses of the parliament which may result in a number of changes if the legislation is passed and becomes law. Also, as the regulations will not be made until the legislation is passed there are some aspects which are not known at this stage as indicated above. Therefore the examples above are based on the bill and indicative of how Division 296 will operate.

Want to know more?

Graeme recently hosted a webinar on this topic which you can watch here.

We will also be hosting more webinars and events with Graeme in the coming months.